Tradingview策略分享1-动量捕捉LRI-STG

视频描述

哈喽小伙伴们,本期带来的是LRI-STG 来源 LRI Momentum Cycles [AlgoAlpha] 感谢原作者开源的代码

本来是一个12月13日更新的指标,我们趁热打铁,做成了策略

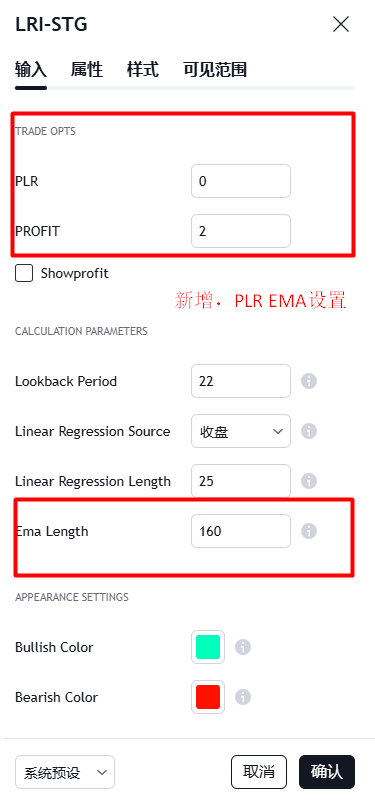

原脚本参数

更改后的参数

默认参数的策略运行效果 时间1小时

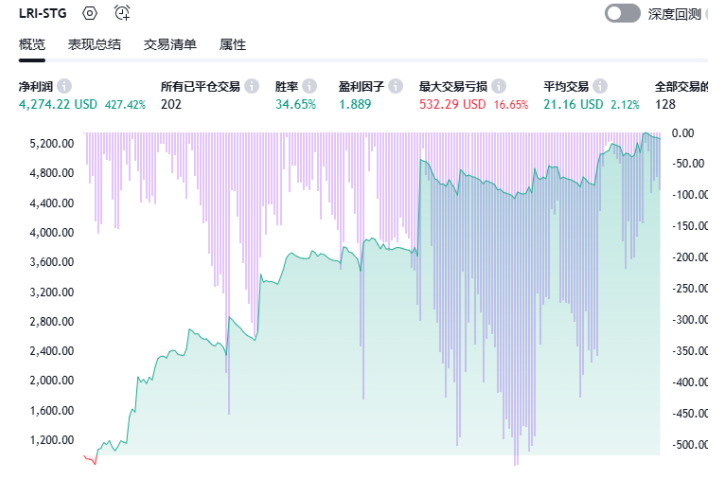

回测效果

SOL 赢利 427%

BCH 375%

FIL 329%

ETH 194%

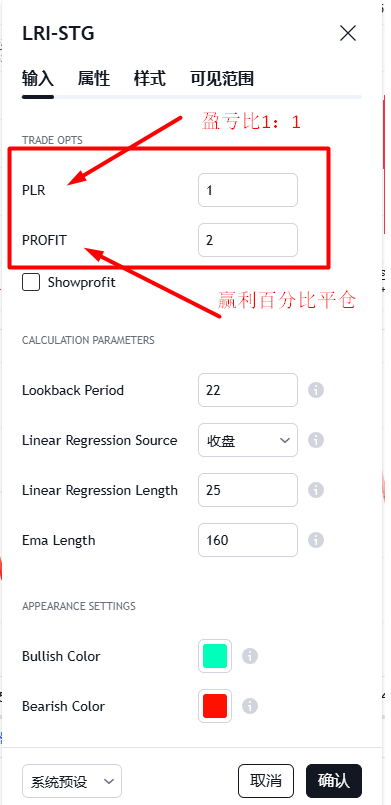

盈亏比设置:

盈亏比设置可以显著增加胜率,但是降低收益,适用于配合短线做高杠杆

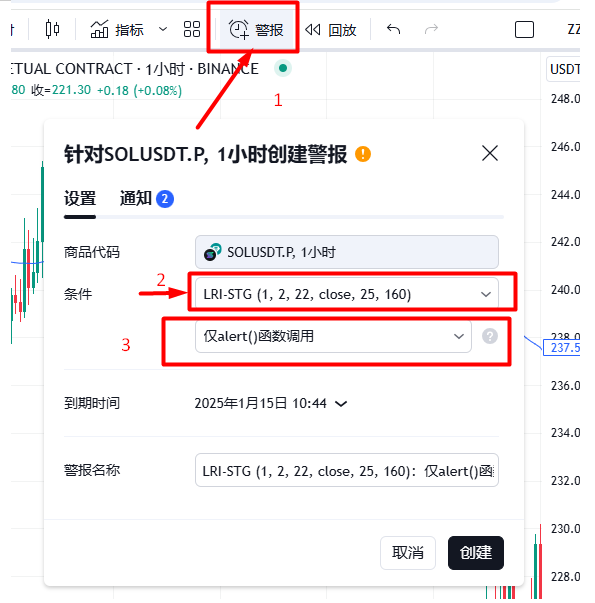

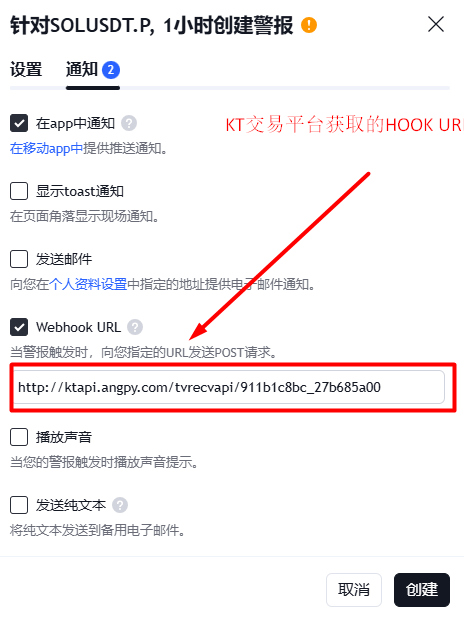

警报设置:

策略集成了KT交易平台,有需要的小伙伴可以注册测试

KT平台复制的hook url

源码下载地址将分享在视频下方链接,您的点赞支持是我长期更新的动力,我们下期见

--------------------------

策略源码:

//@version=5

// indicator("LRI Momentum Cycles [AlgoAlpha]", shorttitle="AlgoAlpha - LRI Momentum", overlay=false)

// upgrader @ktrader2100 date 2024/12/14

strategy(title="LRI-STG", overlay=false, currency="USD", pyramiding=0,

default_qty_type = strategy.cash, calc_on_every_tick = false, initial_capital=1000)

version = '1.1'

symbol_name = syminfo.tickerid

ASSETS = strategy.initial_capital

INIT_USDT_UNIT = ASSETS

// KT INIT START...

PLR = input.float(0, 'PLR', minval=0, step=0.1, group='Trade Opts')

PROFIT = input.float(1, 'PROFIT', minval=0, step=0.1, group='Trade Opts')

showprofit = input.bool(false, "showprofit", group='Trade Opts')

//-----------------------------------------------------------------------------}

//UDT's

//-----------------------------------------------------------------------------{

type ktraderes

float profit

float profit_p

string opt

string ptime

float amount

float usdt_amount

float open_price

float pprice

string debuginfo

float stoplose

float takeprofit

type ktorder

string type

int time

string timedate

string ptime

float pt

float currency

float price

float pprice

float profit

string msg

float stoplose

float takeprofit

//-----------------------------------------------------------------------------}

//Variables

//-----------------------------------------------------------------------------{

varip orders = array.new()

//-----------------------------------------------------------------------------}

//Methods - functions

//-

getTradeResult(string ptime, float price) =>

orderlen = orders.size()

float Ebamount = 0

float Esamount = 0

float Ebcurrency = 0

float Escurrency = 0

Eshow = ''

tradeopt = 'none'

float amount = 0

float open_price = 0

float profit = 0

float profit_p = 0

if orderlen > 0

for i = 0 to orderlen -1

dfrow = orders.get(i)

if dfrow.type == 'buy'

Ebamount := Ebamount + float(dfrow.currency) / float(dfrow.price)

Ebcurrency := Ebcurrency + float(dfrow.currency)

else

Esamount := Esamount + float(dfrow.currency) / float(dfrow.price)

Escurrency := Escurrency + float(dfrow.currency)

if Ebamount > 0 and Esamount > 0

if Ebamount > Esamount

tradeopt := 'buy'

amount := Ebamount - Esamount

else

tradeopt := 'sell'

amount := Esamount - Ebamount

else

if Ebamount > 0

tradeopt := 'buy'

amount := Ebamount

else if Esamount > 0

tradeopt := 'sell'

amount := Esamount

if tradeopt != 'none'

if tradeopt == 'buy'

profit := amount * price - (Ebcurrency - Escurrency)

else

profit := (Escurrency - Ebcurrency) - (amount * price)

// if profit != 0

if tradeopt == 'buy'

profit_p := profit / (Ebcurrency - Escurrency) * 100

else if tradeopt == 'sell'

profit_p := profit / (Escurrency - Ebcurrency) * 100

debuginfo = "Escurrency: " + str.tostring(Escurrency) + "Ebcurrency: " + str.tostring(Ebcurrency)

float stoplose = 0

float takeprofit = 0

if orderlen == 1

stoplose := orders.get(0).stoplose

takeprofit := orders.get(0).takeprofit

res = ktraderes.new(debuginfo = debuginfo, profit = profit, profit_p = profit_p, pprice = price,

amount = amount, opt = tradeopt, open_price = open_price, ptime = ptime, stoplose = stoplose, takeprofit = takeprofit)

res

transTimeToTimedate(int transtime, int ghour)=>

needtranstime = transtime

if transtime == 0

needtranstime := time

gmt = ghour > 0 ? 'GMT+'+str.tostring(ghour) : 'GMT'

timedate = str.format_time(int(needtranstime), "yyyy-MM-dd HH:mm:ss", gmt)

timedate

nowstr = transTimeToTimedate(0, 8)

addOrder(optype, currency, price, addtime, timedate, msg="减仓", stoplose=0, takeprofit=0)=>

tdres = getTradeResult(nowstr, close)

canopt = true

if tdres.opt != 'none'

if tdres.opt == optype

canopt := false

if canopt == true

// label.new(bar_index + 10, 1, optype, size = size.small, color = color.rgb(116, 8, 8))

neworder = ktorder.new(type = optype, currency = currency, price = price, time = addtime, timedate = timedate, msg = msg, stoplose=stoplose, takeprofit=takeprofit)

if optype == 'buy'

strategy.order("buy", strategy.long, qty = currency / price, comment = msg)

else if optype == 'sell'

strategy.order("sell", strategy.short, qty = currency / price, comment = msg)

orders.push(neworder)

pushmsg(string tradecon, float tradeconprice, string side, float price, float currency, float stoplose = 0 , float takeprofit = 0) =>

msgstring = '{"tradecon": "'+tradecon+'", "tradeconprice": "'+str.tostring(tradeconprice)+'", "side": "'+side+'", "price": "'+str.tostring(price)+'", "currency": "'+str.tostring(currency)+'", "stoplose": "'+str.tostring(stoplose)+'", "takeprofit": "'+str.tostring(takeprofit)+'" , "symbol_name": "'+symbol_name+'"}'

alert(message = msgstring, freq = alert.freq_once_per_bar)

''

print_profit(atprice) =>

if showprofit == true

orderl = orders.size()

int i = 0

showtext = ""

showcolumns = array.from("type", "price", "currency", "stop", "take","time", "msg")

showtext := array.join(showcolumns, ",") + "n"

ktres = getTradeResult(transTimeToTimedate(0, 8), close)

while i < orders.size()

corder = orders.get(i)

jarr = array.from(corder.type, str.tostring(corder.price), str.tostring(corder.currency), str.tostring(corder.stoplose), str.tostring(corder.takeprofit), corder.timedate, corder.msg)

rowstr = jarr.join(',')

if str.length(showtext) > 1000

showtext += "n..."

// last line dump

lastlinenum = orders.size() - 1

corder := orders.get(orders.size() - 1)

jarr := array.from(corder.type, str.tostring(corder.price), str.tostring(corder.currency), str.tostring(corder.stoplose), str.tostring(corder.takeprofit), corder.timedate, corder.msg)

rowstr := jarr.join(',')

showtext += ("n" + str.tostring(lastlinenum) + '#' + rowstr)

break

showtext += ("n" + str.tostring(i) + '#' + rowstr)

i += 1

''

resshowstr = "n res:---" + ktres.opt + "n profit:" + str.tostring(ktres.profit) + "n amount:" +

str.tostring(ktres.amount) + "n pprice:" + str.tostring(ktres.pprice)+

"n profit_p: " + str.tostring(ktres.profit_p)

label.new(bar_index, atprice, showtext + resshowstr, size = size.small, color = color.white)

''

// KT INIT END...

calc_group = "Calculation Parameters"

appearance_group = "Appearance Settings"

alerts_group = "Alert Conditions"

n = input.int(22, title="Lookback Period", minval=1, group=calc_group, tooltip="Number of historical bars to analyze")

linreg_source = input.source(close, title="Linear Regression Source", group=calc_group, tooltip="Source for the linear regression calculation")

linreg_length = input.int(25, title="Linear Regression Length", minval=1, group=calc_group, tooltip="Number of bars used for linear regression")

ema_length = input.int(160, title="Ema Length", minval=1, group=calc_group, tooltip="Number of bars used for linear regression")

green = input.color(#00ffbb, title="Bullish Color", group=appearance_group, tooltip="Color when trend is bullish")

red = input.color(#ff1100, title="Bearish Color", group=appearance_group, tooltip="Color when trend is bearish")

v = ta.linreg(linreg_source, linreg_length, 0)

trend = 0

for i = 0 to n - 2

for j = i + 1 to n - 1

if v[i] != v[j]

trend += v[i] > v[j] ? 1 : -1

state = trend > trend[1] or (trend == trend[1] and trend > 0) ? 1 : -1

trendN = trend / ((n * (n - 1)) / 2)

trendColor = state == 1

? color.from_gradient(trendN, 0, 1, color.new(green, 80), color.new(green, 0))

: color.from_gradient(trendN, -1, 0, color.new(red, 0), color.new(red, 80))

p1 = plot(trendN, color=trendColor, linewidth=2, style=plot.style_linebr, title="Trend Normalized")

p2 = plot(trendN[1], display=display.none, title="Previous Trend Normalized")

baseLine = plot(0, color=color.new(color.gray, 90), title="Baseline")

fillColor = state == 1

? color.from_gradient(trendN, 0, 1, color.new(green, 80), color.new(green, 0))

: color.from_gradient(trendN, -1, 0, color.new(red, 0), color.new(red, 80))

fill(p1, p2, fillColor)

// alertcondition(state == 1 and state[1] == -1, title="Bullish Signal", message="Trend turned bullish")

// alertcondition(state == -1 and state[1] == 1, title="Bearish Signal", message="Trend turned bearish")

ema_value = ta.ema(close, ema_length)

ema_slope = ema_value - ta.ema(close[1], ema_length)

plot(ema_value, "EMA", force_overlay = true)

is_uptrend = ema_slope > 0

is_downtrend = ema_slope < 0

tradeopt = 'none'

float stoplose = 0

float takeprofit = 0

// float mvatr = ta.atr(patrlen) * patrmtl

float mvatr = close * PROFIT / 100

tdres = getTradeResult(nowstr, close)

buycon = state == 1 and state[1] == -1 and is_uptrend

sellcon = state == -1 and state[1] == 1 and is_downtrend

// plot(state , title = 'state')

// plot(buycon ? 1 : 0 , title = 'buycon')

// plot(sellcon ? 1 : 0 , title = 'sellcon')

if buycon

//label.new(bar_index, state, tdres.opt, size = size.small, color = color.rgb(158, 56, 56))

tradeopt := 'buy'

if tdres.opt == 'sell'

strategy.close_all()

orders := array.new(0)

tdres := getTradeResult(nowstr, close)

//label.new(bar_index + 5, state, tdres.opt, size = size.small, color = #b10d0d)

if tdres.opt == 'none'

if PLR > 0 and PROFIT > 0

float mvatr2 = close + (close * PROFIT / 100)

stoplose := close - mvatr / PLR

takeprofit := close + mvatr

label.new(bar_index, takeprofit, 'probuy:' + str.tostring(mvatr), size = size.small, color = #b10d0d,force_overlay = true)

else

stoplose := 0

takeprofit := 0

addOrder(optype = tradeopt, currency = INIT_USDT_UNIT, price = close, addtime=time,

timedate = nowstr, msg='开多',

stoplose = stoplose, takeprofit = takeprofit)

pushmsg(tradecon='<',

tradeconprice=close,

side='buy',

price=close,

currency=1,

stoplose = stoplose,

takeprofit = takeprofit)

if sellcon

tradeopt := 'sell'

if tdres.opt == 'buy'

strategy.close_all()

orders := array.new(0)

tdres := getTradeResult(nowstr, close)

if tdres.opt == 'none'

if PLR > 0 and PROFIT > 0

stoplose := close + mvatr / PLR

takeprofit := close - mvatr

else

stoplose := 0

takeprofit := 0

addOrder(optype = tradeopt, currency = INIT_USDT_UNIT, price = close,

addtime=time, timedate = nowstr, msg='开空',

stoplose = stoplose, takeprofit = takeprofit)

pushmsg(tradecon='>',

tradeconprice=close,

side='sell',

price=close,

currency=1,

stoplose = stoplose,

takeprofit = takeprofit)

if PLR > 0

if tdres.opt != 'none'

if tdres.profit > 0

if tdres.opt == 'buy'

if close >= tdres.takeprofit

strategy.close_all(comment = '多单止盈')

orders := array.new(0)

else if tdres.opt == 'sell'

if close <= tdres.takeprofit

strategy.close_all(comment = '空单止盈')

orders := array.new(0)

else if tdres.profit < 0

if tdres.opt == 'buy'

if close <= tdres.stoplose

strategy.close_all(comment = '多单止损')

orders := array.new(0)

else if tdres.opt == 'sell'

if close >= tdres.stoplose

strategy.close_all(comment = '空单止损')

orders := array.new(0)

if barstate.islastconfirmedhistory

print_profit(0)