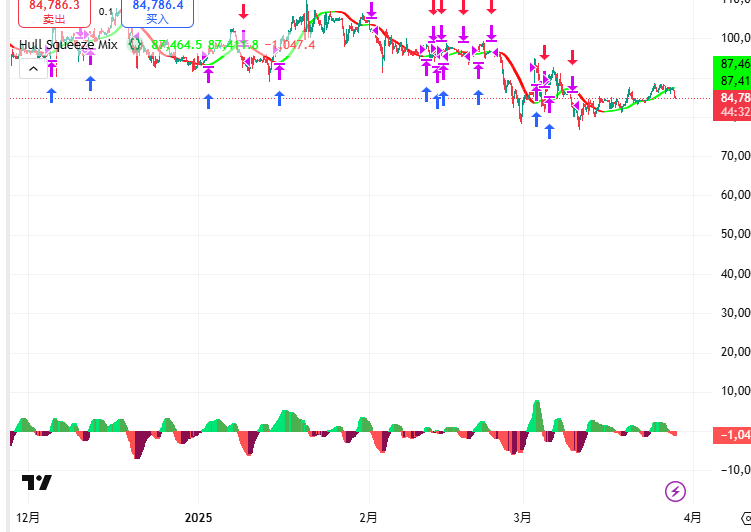

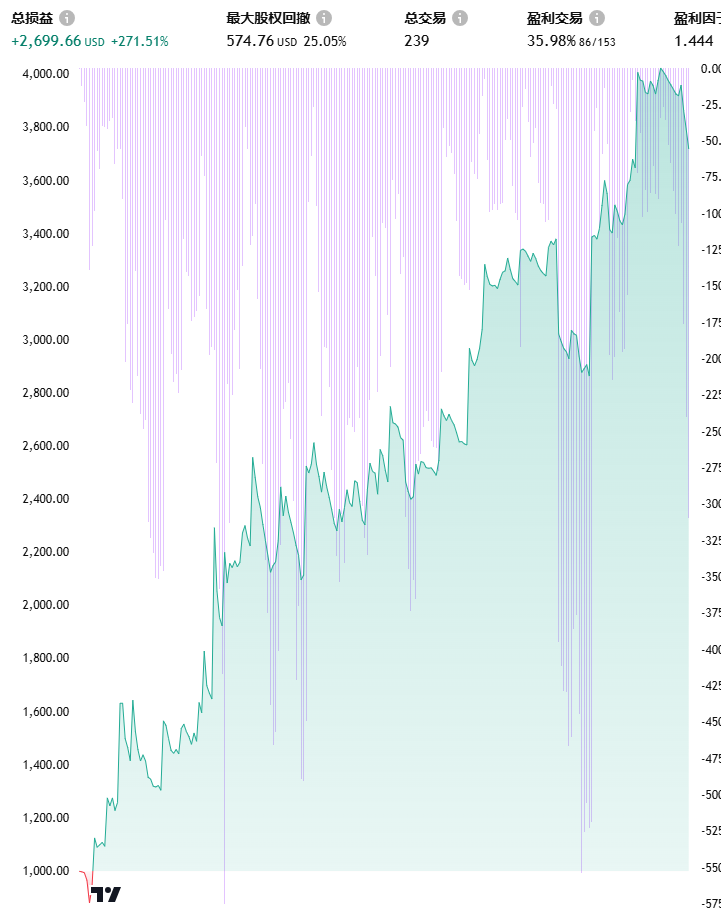

策略效果:

BTC 策略曲线

少有对BTC 交易赢利曲线平滑的策略

上源码:

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © ktrader2100

//@version=5

// use 4h

strategy(title="Hull Squeeze Mix", overlay=true, currency="USD", pyramiding=0,

default_qty_type=strategy.cash, calc_on_every_tick=true, initial_capital=1000)

v = 1.1

// Hull Suite by InSilico

//INPUT

src = input(close, title="Source")

modeSwitch = input.string("Hma", title="Hull Variation", options=["Hma", "Thma", "Ehma"])

length = input(110, title="Length(180-200 for floating S/R , 55 for swing entry)")

lengthMult = input(1.0, title="Length multiplier (Used to view higher timeframes with straight band)")

useHtf = input(false, title="Show Hull MA from X timeframe? (good for scalping)")

htf = input.timeframe("240", title="Higher timeframe")

switchColor = input(true, "Color Hull according to trend?")

candleCol = input(false,title="Color candles based on Hull's Trend?")

visualSwitch = input(true, title="Show as a Band?")

thicknesSwitch = input(1, title="Line Thickness")

transpSwitch = input.int(40, title="Band Transparency",step=5)

//FUNCTIONS

//HMA

HMA(_src, _length) => ta.wma(2 * ta.wma(_src, _length / 2) - ta.wma(_src, _length), math.round(math.sqrt(_length)))

//EHMA

EHMA(_src, _length) => ta.ema(2 * ta.ema(_src, _length / 2) - ta.ema(_src, _length), math.round(math.sqrt(_length)))

//THMA

THMA(_src, _length) => ta.wma(ta.wma(_src,_length / 3) * 3 - ta.wma(_src, _length / 2) - ta.wma(_src, _length), _length)

//SWITCH

Mode(modeSwitch, src, len) =>

modeSwitch == "Hma" ? HMA(src, len) :

modeSwitch == "Ehma" ? EHMA(src, len) :

modeSwitch == "Thma" ? THMA(src, len/2) : na

//OUT

_hull = Mode(modeSwitch, src, int(length * lengthMult))

HULL = useHtf ? request.security(syminfo.ticker, htf, _hull) : _hull

MHULL = HULL[0]

SHULL = HULL[2]

//COLOR

hullColor = switchColor ? (HULL > HULL[2] ? #00ff00 : #ff0000) : #ff9800

//PLOT

///< Frame

Fi1 = plot(MHULL, title="MHULL", color=hullColor, linewidth=thicknesSwitch)

Fi2 = plot(visualSwitch ? SHULL : na, title="SHULL", color=hullColor, linewidth=thicknesSwitch)

alertcondition(ta.crossover(MHULL, SHULL), title="Hull trending up.", message="Hull trending up.")

alertcondition(ta.crossover(SHULL, MHULL), title="Hull trending down.", message="Hull trending down.")

///< Ending Filler

fill(Fi1, Fi2, title="Band Filler", color=hullColor)

///BARCOLOR

barcolor(color = candleCol ? (switchColor ? hullColor : na) : na)

// Squeeze Momentum Indicator

// 输入参数

length2 = input.int(20, title="BB Length")

mult = input.float(5, title="BB MultFactor")

lengthKC = input.int(21, title="KC Length")

multKC = input.float(1.5, title="KC MultFactor")

useTrueRange = input.bool(true, title="Use TrueRange (KC)")

// 计算布林带 (BB)

source = close

basis = ta.sma(source, length2)

dev = multKC * ta.stdev(source, length2)

upperBB = basis + dev

lowerBB = basis - dev

// 计算肯特纳通道 (KC)

ma = ta.sma(source, lengthKC)

range1 = useTrueRange ? ta.tr : (high - low)

rangema = ta.sma(range1, lengthKC)

upperKC = ma + rangema * multKC

lowerKC = ma - rangema * multKC

// 确定挤压状态

sqzOn = (lowerBB > lowerKC) and (upperBB < upperKC)

sqzOff = (lowerBB < lowerKC) and (upperBB > upperKC)

noSqz = not sqzOn and not sqzOff

// 计算动量

val = ta.linreg(source - math.avg(math.avg(ta.highest(high, lengthKC), ta.lowest(low, lengthKC)), ta.sma(close, lengthKC)),

lengthKC, 0)

// 设置柱状图颜色

bcolor = val > 0 ? (val > nz(val[1]) ? color.lime : color.green)

: (val < nz(val[1]) ? color.red : color.maroon)

// 设置零线颜色

scolor = noSqz ? color.blue : sqzOn ? color.black : color.gray

// 绘制图表

plot(val, color=bcolor, style=plot.style_histogram, linewidth=4)

// plot(0, color=scolor, style=plot.style_cross, linewidth=2)

// KT STGS

symbol_name = syminfo.tickerid

// kt stgs start ...

var LQ_RATIO = 0.6

INIT_USDT_UNIT = strategy.initial_capital

PLR = input.float(0, 'PLR', minval=0, step=0.1, group='KT Trade Opts')

showprofit = input.bool(false, "showprofit", group='KT Trade Opts')

check100xlist = array.new_string(0, '')

if barstate.isfirst

check100xlist.push('BTCUSDT')

check100xlist.push('ETHUSDT')

check100xlist.push('SOLUSDT')

for i = 0 to array.size(check100xlist) - 1

strValue = array.get(check100xlist, i)

if str.contains(symbol_name, strValue)

LQ_RATIO := 0.6

break

LQ_RATIO := 0.8

// plot(LQ_RATIO, title = 'LQ_RATIO')

//-----------------------------------------------------------------------------}

//UDT's

//-----------------------------------------------------------------------------{

type ktraderes

float profit

float profit_p

string opt

string ptime

float amount

float usdt_amount

float open_price

float pprice

string debuginfo

float stoplose

float takeprofit

type ktorder

string type

int time

string timedate

string ptime

float pt

float currency

float price

float pprice

float profit

string msg

float stoplose

float takeprofit

//-----------------------------------------------------------------------------}

//Variables

//-----------------------------------------------------------------------------{

varip orders = array.new<ktorder>()

//Methods - functions

//-

method n(float piv) => bool out = not na(piv)

pushmsg(string tradecon, float tradeconprice, string side, float price, float currency, float stoplose = 0 , float takeprofit = 0) =>

// strtpl = '{"tradecon": ">", "tradeconprice": "92946", "side": "sell", "price": "92946", "currency": "5000", "stoplose": "0", "takeprofit": "0"}'

// strtpl = "{"tradecon": {0}, "tradeconprice": "{1}", "side": "{2}", "price": "{3}", "currency": "{4}", "stoplose": "{5}", "takeprofit": "{6}"}'

msgstring = '{"tradecon": "'+tradecon+'", "tradeconprice": "'+str.tostring(tradeconprice)+'", "side": "'+side+'", "price": "'+str.tostring(price)+'", "currency": "'+str.tostring(currency)+'", "stoplose": "'+str.tostring(stoplose)+'", "takeprofit": "'+str.tostring(takeprofit)+'" , "symbol_name": "'+symbol_name+'"}'

// msgstring = str.format(strtpl, tradecon)

alert(message = msgstring, freq = alert.freq_once_per_bar)

''

getTradeResult(string ptime, float price) =>

orderlen = orders.size()

float Ebamount = 0

float Esamount = 0

float Ebcurrency = 0

float Escurrency = 0

Eshow = ''

tradeopt = 'none'

float amount = 0

float open_price = 0

float profit = 0

float profit_p = 0

if orderlen > 0

for i = 0 to orderlen -1

dfrow = orders.get(i)

if dfrow.type == 'buy'

Ebamount := Ebamount + float(dfrow.currency) / float(dfrow.price)

Ebcurrency := Ebcurrency + float(dfrow.currency)

else

Esamount := Esamount + float(dfrow.currency) / float(dfrow.price)

Escurrency := Escurrency + float(dfrow.currency)

if Ebamount > 0 and Esamount > 0

if Ebamount > Esamount

tradeopt := 'buy'

amount := Ebamount - Esamount

else

tradeopt := 'sell'

amount := Esamount - Ebamount

else

if Ebamount > 0

tradeopt := 'buy'

amount := Ebamount

else if Esamount > 0

tradeopt := 'sell'

amount := Esamount

if tradeopt != 'none'

if tradeopt == 'buy'

profit := amount * price - (Ebcurrency - Escurrency)

else

profit := (Escurrency - Ebcurrency) - (amount * price)

// if profit != 0

if tradeopt == 'buy'

profit_p := profit / (Ebcurrency - Escurrency) * 100

else if tradeopt == 'sell'

profit_p := profit / (Escurrency - Ebcurrency) * 100

debuginfo = "Escurrency: " + str.tostring(Escurrency) + "Ebcurrency: " + str.tostring(Ebcurrency)

float stoplose = 0

float takeprofit = 0

if orderlen == 1

stoplose := orders.get(0).stoplose

takeprofit := orders.get(0).takeprofit

res = ktraderes.new(debuginfo = debuginfo, profit = profit, profit_p = profit_p, pprice = price,

amount = amount, opt = tradeopt, open_price = open_price, ptime = ptime, stoplose = stoplose, takeprofit = takeprofit)

res

transTimeToTimedate(int transtime, int ghour)=>

needtranstime = transtime

if transtime == 0

needtranstime := time

gmt = ghour > 0 ? 'GMT+'+str.tostring(ghour) : 'GMT'

timedate = str.format_time(int(needtranstime), "yyyy-MM-dd HH:mm:ss", gmt)

timedate

nowstr = transTimeToTimedate(0, 8)

addOrder(optype, currency, price, time, timedate, msg="减仓", stoplose=0, takeprofit=0)=>

tdres = getTradeResult(nowstr, close)

canopt = true

if tdres.opt != 'none'

if tdres.opt == optype

canopt := false

if canopt == true

neworder = ktorder.new(type = optype, currency = currency, price = price, time = time, timedate = timedate, msg = msg, stoplose=stoplose, takeprofit=takeprofit)

if optype == 'buy'

strategy.order("buy", strategy.long, qty = currency / price, comment = msg)

else if optype == 'sell'

strategy.order("sell", strategy.short, qty = currency / price, comment = msg)

orders.push(neworder)

print_profit(atprice) =>

if showprofit == true

orderl = orders.size()

int i = 0

showtext = ""

showcolumns = array.from("type", "price", "currency", "stop", "take","time", "msg")

showtext := array.join(showcolumns, ",") + "n"

ktres = getTradeResult(transTimeToTimedate(0, 8), close)

while i < orders.size()

corder = orders.get(i)

jarr = array.from(corder.type, str.tostring(corder.price), str.tostring(corder.currency), str.tostring(corder.stoplose), str.tostring(corder.takeprofit), corder.timedate, corder.msg)

rowstr = jarr.join(',')

if str.length(showtext) > 1000

showtext += "n..."

// last line dump

lastlinenum = orders.size() - 1

corder := orders.get(orders.size() - 1)

jarr := array.from(corder.type, str.tostring(corder.price), str.tostring(corder.currency), str.tostring(corder.stoplose), str.tostring(corder.takeprofit), corder.timedate, corder.msg)

rowstr := jarr.join(',')

showtext += ("n" + str.tostring(lastlinenum) + '#' + rowstr)

break

showtext += ("n" + str.tostring(i) + '#' + rowstr)

i += 1

''

resshowstr = "n res:---" + ktres.opt + "n profit:" + str.tostring(ktres.profit) + "n amount:" +

str.tostring(ktres.amount) + "n pprice:" + str.tostring(ktres.pprice)+

"n profit_p: " + str.tostring(ktres.profit_p)

label.new(bar_index, atprice, showtext + resshowstr, size = size.small, color = color.white)

''

// todo starts ....

buycon = false

sellcon = false

tdres = getTradeResult(nowstr, close)

pmsg = false

tradeopt = 'none'

float stoplose = 0

float takeprofit = 0

// todo cac...

// alertcondition(ta.crossover(MHULL, SHULL), title="Hull trending up.", message="Hull trending up.")

// alertcondition(ta.crossover(SHULL, MHULL), title="Hull trending down.", message="Hull trending down.")

// bcolor = val > 0 ? (val > nz(val[1]) ? color.lime : color.green)

// : (val < nz(val[1]) ? color.red : color.maroon)

if ta.crossover(MHULL, SHULL) and val > nz(val[1])

buycon := true

if ta.crossover(SHULL, MHULL) and val < nz(val[1])

sellcon := true

// todo cac end...

if buycon

tradeopt := 'buy'

if tdres.opt == 'sell'

strategy.close_all()

orders := array.new<ktorder>(0)

tdres := getTradeResult(nowstr, close)

if tdres.opt == 'none'

if PLR > 0

mv = close * LQ_RATIO / 100

stoplose := close - mv

takeprofit := close + mv * PLR

else

stoplose := 0

takeprofit := 0

currency = INIT_USDT_UNIT

mcurrency = 1

msg='开多'

addOrder(optype = tradeopt, currency = currency, price = close, time=time,

timedate = nowstr, msg=msg,

stoplose = stoplose, takeprofit = takeprofit)

pushmsg(tradecon='<',

tradeconprice=close,

side='buy',

price=close,

currency=mcurrency,

stoplose = 0,

takeprofit = 0)

if sellcon

tradeopt := 'sell'

if tdres.opt == 'buy'

strategy.close_all()

orders := array.new<ktorder>(0)

tdres := getTradeResult(nowstr, close)

if tdres.opt == 'none'

if PLR > 0

mv = close * LQ_RATIO / 100

stoplose := close + mv

takeprofit := close - mv * PLR

else

stoplose := 0

takeprofit := 0

currency = INIT_USDT_UNIT

mcurrency = 1

msg='开空'

addOrder(optype = tradeopt, currency = currency, price = close,

time=time, timedate = nowstr, msg=msg,

stoplose = stoplose, takeprofit = takeprofit)

pushmsg(tradecon='>',

tradeconprice=close,

side='sell',

price=close,

currency=mcurrency,

stoplose = 0,

takeprofit = 0)

// plot(orders.size(), 'ordersize')

// plot(close, title = "tickprice")

if barstate.islastconfirmedhistory

print_profit(0)